Page 30 - Nexia Cape Town 2018 TG Digital

P. 30

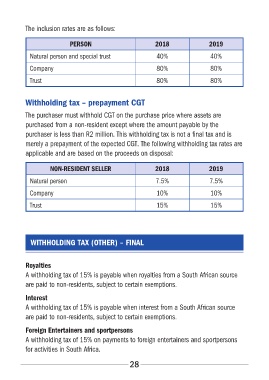

The inclusion rates are as follows:

PERSON 2018 2019

Natural person and special trust 40% 40%

Company 80% 80%

Trust 80% 80%

Withholding tax – prepayment CGT

The purchaser must withhold CGT on the purchase price where assets are

purchased from a non-resident except where the amount payable by the

purchaser is less than R2 million� This withholding tax is not a final tax and is

merely a prepayment of the expected CGT� The following withholding tax rates are

applicable and are based on the proceeds on disposal:

NON-RESIDENT SELLER 2018 2019

Natural person 7�5% 7�5%

Company 10% 10%

Trust 15% 15%

WITHHOLDING TAX (OTHER) – FINAL

Royalties

A withholding tax of 15% is payable when royalties from a South African source

are paid to non-residents, subject to certain exemptions�

Interest

A withholding tax of 15% is payable when interest from a South African source

are paid to non-residents, subject to certain exemptions�

Foreign Entertainers and sportpersons

A withholding tax of 15% on payments to foreign entertainers and sportpersons

for activities in South Africa�

28