Page 12 - Nexia Cape Town 2018 TG Digital

P. 12

DEDUCTIONS

Contributions to pension, provident and retirement annuity funds

With effect 1 March 2016 the tax deduction for contributions made to pension

funds, provident funds and retirement annuity funds is significantly amended�

Please refer to previous year’s tax guides for the tax treatment before 1 March

2016� From 1 March 2016 onwards, the tax deduction calculation for the three

different funds, pension, provident and retirement annuity funds will be identical�

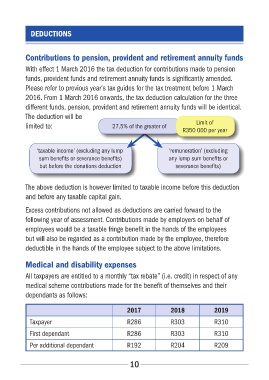

The deduction will be

limited to: 27,5% of the greater of Limit of

R350 000 per year

‘taxable income’ (excluding any lump ‘remuneration’ (excluding

sum benefits or severance benefits) any lump sum benefits or

but before the donations deduction severance benefits)

The above deduction is however limited to taxable income before this deduction

and before any taxable capital gain�

Excess contributions not allowed as deductions are carried forward to the

following year of assessment� Contributions made by employers on behalf of

employees would be a taxable fringe benefit in the hands of the employees

but will also be regarded as a contribution made by the employee, therefore

deductible in the hands of the employee subject to the above limitations�

Medical and disability expenses

All taxpayers are entitled to a monthly “tax rebate” (i�e� credit) in respect of any

medical scheme contributions made for the benefit of themselves and their

dependants as follows:

2017 2018 2019

Taxpayer R286 R303 R310

First dependant R286 R303 R310

Per additional dependant R192 R204 R209

10