Page 8 - Nexia Cape Town 2018 TG Digital

P. 8

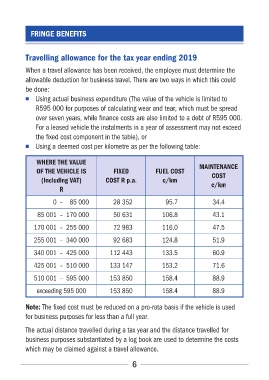

FRINGE BENEFITS

Travelling allowance for the tax year ending 2019

When a travel allowance has been received, the employee must determine the

allowable deduction for business travel� There are two ways in which this could

be done:

■ Using actual business expenditure (The value of the vehicle is limited to

R595 000 for purposes of calculating wear and tear, which must be spread

over seven years, while finance costs are also limited to a debt of R595 000�

For a leased vehicle the instalments in a year of assessment may not exceed

the fixed cost component in the table), or

■ Using a deemed cost per kilometre as per the following table:

WHERE THE VALUE MAINTENANCE

OF THE VEHICLE IS FIXED FUEL COST COST

(Including VAT) COST R p.a. c/km c/km

R

0 – 85 000 28 352 95�7 34�4

85 001 – 170 000 50 631 106�8 43�1

170 001 – 255 000 72 983 116�0 47�5

255 001 – 340 000 92 683 124�8 51�9

340 001 – 425 000 112 443 133�5 60�9

425 001 – 510 000 133 147 153�2 71�6

510 001 – 595 000 153 850 158�4 88�9

exceeding 595 000 153 850 158�4 88�9

Note: The fixed cost must be reduced on a pro-rata basis if the vehicle is used

for business purposes for less than a full year�

The actual distance travelled during a tax year and the distance travelled for

business purposes substantiated by a log book are used to determine the costs

which may be claimed against a travel allowance�

6